A Friendly and Important Disclaimer Note (in

addition to legal language below): If you’re reading this post and are not currently investing with Soos Global (which, of course, is

something we should discuss!), please bear in mind that while we share details

on changes made to our portfolios, it's important to consider that our

portfolio decisions are taken in a much broader context of our overall

portfolio strategies and our assessment of each of our investor's unique

financial profiles. As such, what we do, and when we do it, is specific

to our investor portfolios and is NOT intended, in any way, as advice for use

by others. Readers are reminded that all comments posted here are for information

and entertainment purposes only!

Any commentary, especially those that include specific mentions of

'buying' or 'selling' or 'positions', is made solely for those limited

informational and entertainment purposes, and NOT as advice.

Thanks for reading. And please

email or call w/any questions or to discuss in more detail. Also,

please visit http://stockcharts.com/public/1587236

to see our charts of close to 100 stocks/etfs on our radar screen.

Best, Ed

(If you'd like to exchange thoughts on this post or on other subjects, please connect with me through the Private Chat tool on the right side of this page, or if you'd like to email thoughts, please do so through the Contact Form feature. For public airings, please use the Comment feature below. Looking forward to hearing your thoughts!)

(If you'd like to exchange thoughts on this post or on other subjects, please connect with me through the Private Chat tool on the right side of this page, or if you'd like to email thoughts, please do so through the Contact Form feature. For public airings, please use the Comment feature below. Looking forward to hearing your thoughts!)

(Below is a note sent to investors yesterday as part of our ongoing regular portfolio updates..fyi).

Just a quick update on the portfolio and market thoughts.

You'll recall that in late September, I moved some of our

cash position into fixed income ETFs with the thought that the market was

overly pessimistic about interest rates rising. Given the capacity

excesses both in terms of labor and other means of production, it seemed then,

and continues to seem to me now that long-term interest rates would be unlikely

to spike higher any time soon. Yes, with the Fed having completed QE and

with the US economy continuing to show some signs of life, especially in the

labor market, the market is correct to anticipate a move upwards in short-term

rates by the Fed, but anything more than a small, deliberate move would not be

in sync, in my opinion, with the economic realities. In particular,

while the Fed minutes of late have made a big deal of the improving labor

market, the reality is that job growth of roughly 200k per month is still only

a 'slow' pace of job growth and would really need to be over 300k per month to

make a serious dent in the un- and under-employed numbers which then could

trigger some meaningful wage pressures. Until then, it's not surprising

that wage growth has remained stagnant.

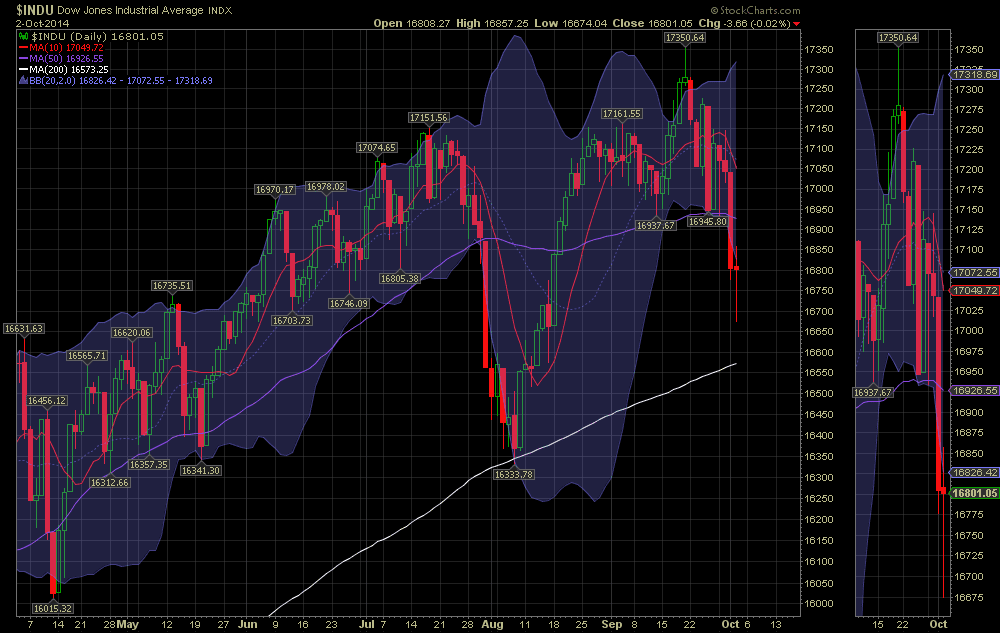

As we continue to be in an environment where equity markets

are at or near all-time highs, where earnings are likely to have trouble

keeping pace with previous quarterly gains, where Japan has recently been

confirmed to be in recession and where Europe continues to struggle

economically (in addition to geopolitically with Russia/Ukraine on its

doorstep), I continue to believe that putting some portion of the portfolio in

income producing assets makes sense, and, as I've been doing when specific

equities retreat to more compelling valuations, using our cash, or money that

is in fixed income ETFs, to then purchase more equities.

Currently, I'm considering adding some preferred bond/stock

ETFs to the mix. Their yields are north of 5%, they trade generally

with less volatility, and the credit quality of the companies appears to be

good. I'm also looking to add some of the fixed income ETFs that

we already have.

As for equities, I continue to position the portfolio around

our key global macro themes, most notably being the global emergence of middle

class consumers in a growing number of countries around the world. While

we have many successes in the diversified mix, and I'd be delighted to discuss

them with you any time, I do want to comment on some of the 'hot spots' in the

portfolio so that you're up to date on my tactical and strategic plans:

XLE, TAN: The rout in oil prices has put

pressure on our XLE etf, and our solar etf whose ticker is TAN. I

believe that oil prices will bounce from current levels, so I expect to hold

both for now, but I'm considering selling TAN at higher levels as the

theme of a global move into alternative energy sources should lose some urgency

with oil and natural gas prices having fallen so low. Some M&A

activity in the wind/solar space of late has helped give TAN a boost, but a

more meaningful run up in TAN, I believe, would have to be preceded by a move

up in oil and related companies, which might likely be captured by XLE.

Yamana (AUY)….continues to suffer on weak gold

prices, mostly due to strong USD, but also due to expectations of lower demand

from India as the country looks to slow gold purchases in order to stem the

current account deficit. The stock got hit hard on its last earnings

release which missed expectations and was muddied by higher taxes in Chile and

by problems with their Brazilian mines. Given how low the stock trades,

it could easily be a target by other gold miners as the whole space is

suffering currently from weak global growth, strong USD and ample

supplies. There was talk last week that AUY would spin off their

Brazilian mines, news that the market liked. I plan on holding on and

expect the current extreme negative sentiment in this pace to abate, at which

point, AUY, being a low-cost producer, could stand to do well.

HIMX…has had a hard time recovering from market

expectations that Google Glass is not going to happen. HIMX, being partly

owned by Google, was expected to play a big role in the Google Glass wearable

market. The whole wearable market is still evolving, and I expect HIMX to

be a player in that space. In the meantime, it is not a one-horse

wonder. It's ICs and semis are used in a growing diversity of products

with a growing diversity of customers. The coming months should be

particularly telling as to consumer appetite for 'wearables'. Many new

products are being featured for the upcoming shopping season, and I'd expect

the flurry of activity amongst designers and manufacturers to pick up once the

most compelling versions of the products are identified.

In each of the cases above, I'm keeping a particularly close

eye on how events unfold and will keep you posted if things evolve in a way

that warrants a change in course.

In the meantime, please email or call if you have any

questions.

Best,

Ed

Please continue to visit Soos Global Market Musings for updates.

(Sign up to "Follow by Email"! And share with others!)

(Please note: This article is solely meant to be thought provoking and is not in any way meant to be personal investment advice. Each investor is obligated to opine and decide for themselves as to the appropriateness of anything said in this article to their unique financial profile, risk tolerances and portfolio goals).

Disclaimer: Please read and consider important information related to all communication made by Soos Global on this site by clicking here.

Additional Disclaimer: currently long many stocks/ETFs incl HIMX, AUY, XLE, TAN, PFF, PFXF, PGF. Positions may change at any time without notice.

(Sign up to "Follow by Email"! And share with others!)

(Please note: This article is solely meant to be thought provoking and is not in any way meant to be personal investment advice. Each investor is obligated to opine and decide for themselves as to the appropriateness of anything said in this article to their unique financial profile, risk tolerances and portfolio goals).

Disclaimer: Please read and consider important information related to all communication made by Soos Global on this site by clicking here.

Additional Disclaimer: currently long many stocks/ETFs incl HIMX, AUY, XLE, TAN, PFF, PFXF, PGF. Positions may change at any time without notice.