"Morning Memo" begins below this "NOTE for NEWCOMERS" to "Morning Memo"...... Each

morning, we post a short bullet-point list of noteworthy events,

data, etc that find their way into the assessment of global markets.

It's far from complete and is not meant to be an exhaustive

reconciliation of all things that could possibly impact stocks, bonds,

currencies and commodities! Rather, it's best viewed as a cryptic memo

of "highlights", noteworthy items that took place in Asia, European and

US hours.....and color-coded 'Red' for seemingly negative impact on equity markets, 'Green' for positive.

This will also serve as a useful review mechanism, as scrolling through the series of "Morning Memo" posts over time ought to summarily highlight what generally drove price action.

We hope you find this useful and informative....and as always, that you'll share feedback!!

5:30am, ET....

This will also serve as a useful review mechanism, as scrolling through the series of "Morning Memo" posts over time ought to summarily highlight what generally drove price action.

We hope you find this useful and informative....and as always, that you'll share feedback!!

5:30am, ET....

- Asia...lower, following US markets selloff late yesterday on Secy of State Kerry's comments that the US is considering response to Syria's use of chemical weapons.

- Philippines... catching up to other Asian markets' selloffs in recent days, returned from a holiday on Monday to drop over 4% in early trading. Meanwhile, the Thai Bhat, India's Rupee and Indonesia Rupiah continued under pressure; so hopes that the carnage in emerging country currencies and stocks might be over as Fed tapering has been priced in do not seem to be met yet!

- IPOs (initial public offerings)..Interesting factoid reported in the Financial Times' fastFT, citing Dealogic's data on IPOs: Asia ex-Japan IPO volume is at lowest level since 2005. Hong Kong is an exception, posting higher volumes than last year. Also,

Globally, IPO volumes are up 25 per cent from last year. IPO volume in Europe has done particularly well—it's tripled from last year, to $14.4bn.

- Germany...IFO business confidence survey better than expected! Increases for the fourth consecutive month. (the index is still below its historical high hit in Feb 2011).

- Europe..despite Germany's strong IFO data, the focus on US involvement in Syria is dominating attention and markets are broadly lower.

- US...Treasury Secy Jack Lew says debt limit will be hit in mid-October, roughly one month earlier than had been expected. Puts more pressure on Congress, who returns from recess on September 9, to come up with a debt ceiling deal. (Editorial comment: Bear in mind, in addition to the major issue of the debt ceiling, there's also the major issue of the US fiscal year ending September 30. A continuing resolution to keep paying bills would be needed to avoid shutting down the government! Negotiations on this should be intense).

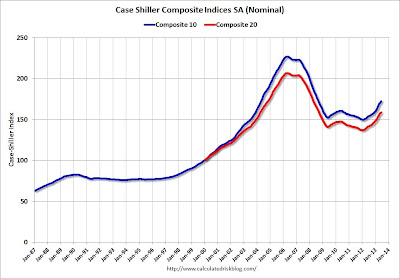

- Case-Shiller Home Price index, up 12.1% y/y, in line w/expectations, but slightly slower on a m/m basis. Still good report on housing front. See CalculatedRiskBlog.com

- more later...

Please continue to visit Soos Global Market Musings for updates.

(Sign up to "Follow by Email"! And share with others!)

(Please note: This article is solely meant to be thought provoking and is not in any way meant to be personal investment advice. Each investor is obligated to opine and decide for themselves as to the appropriateness of anything said in this article to their unique financial profile, risk tolerances and portfolio goals).

Disclaimer: Please read and consider important information related to all communication made by Soos Global on this site by clicking here.

Additional Disclaimer: currently long many stocks/ETFs. Positions may change at any time without notice.

No comments:

Post a Comment